In corporate negotiations, few phrases expedite the execution of commercial contracts as effectively as the assertion that an indemnification clause is mutual. This structural reciprocity often induces a false sense of security among principal stakeholders and founders. Under the assumption of inherent fairness, decision-makers frequently pivot attention to primary commercial terms, treating risk-allocation provisions as settled boilerplate.

This reliance on structural symmetry is fundamentally misplaced. Mutuality dictates the bilateral architecture of a clause, ensuring obligations run in both directions, but fails to account for the volume or velocity of the risk flowing through it. Two indemnity provisions can be perfectly reciprocal in drafting yet profoundly unequal in financial impact. For post-Series A enterprises with substantial recurring revenue, protected cap tables, and enterprise-scale counterparties possessing the capital to litigate, the divergence between formal mutuality and actual risk parity represents a critical, unhedged balance-sheet liability.

This analysis isolates a specific contractual risk: how a facially balanced clause can disproportionately allocate liability to a single party, and the precise mechanics required to identify and mitigate this exposure under Indian law prior to execution.

Defining the Contract of Indemnity

What is indemnity?

An indemnity is a promise to bear another party’s loss. In the contractual setting, an indemnification clause is the provision by which one party (the indemnifier) agrees to compensate the other (the indemnity holder) for specified losses, typically those arising from third-party claims, breaches, or defined risk events. It is, at its core, a mechanism for shifting the financial consequences of a risk from the party that would otherwise bear it to the party the contract designates.

Under Indian law, the contract of indemnity is defined in Section 124 of the Indian Contract Act, 1872, as a contract by which one party promises to save the other from loss caused by the conduct of the promisor himself, or by the conduct of any other person. Section 125 outlines the statutory rights of the indemnity holder when sued, specifying the recovery of:

- All damages compelled to be paid in any suit to which the promise to indemnify applies;

- All costs incurred in bringing or defending such suits, provided the party acted prudently; and

- All sums paid under the terms of any reasonable compromise.

The statutory framework under Section 124 is considerably narrower than modern commercial requirements. Indian courts recognize that commercial parties frequently draft indemnities extending well beyond the default statutory language to capture third-party claims, intellectual property (IP) infringement, data breaches, and regulatory non-compliance. Such provisions are enforced as ordinary contractual obligations under Section 10 of the Act, provided standard requisites of a valid contract are met.

A properly drafted indemnification clause circumvents the statutory limitations governing standard claims for damages under Section 73. While Section 73 excludes indirect, consequential, or remote losses under the rule of foreseeability, a bespoke indemnity provision can be explicitly engineered to cover these broader economic liabilities. This makes the clause inherently more potent than default statutory remedies.

The Structural Reality of Mutual vs. One-Sided Clauses

The Core Definitions

- Mutual Indemnification Clause: A reciprocal provision requiring both parties to indemnify each other on identical legal terms for losses arising from their respective breaches, negligence, or infringements. This framework assumes both sides introduce comparable risk profiles into the transaction.

- One-Sided Indemnification Clause: A unilateral provision placing the entire indemnity obligation upon a single party. This is the standard operational structure where one party inherently introduces the primary risk into the commercial relationship (e.g., a software vendor providing an IP indemnity to a corporate buyer).

Legal Mechanics Underpinning the Risk

Two foundational features of Indian jurisprudence govern how a mutual indemnification clause operates in practice, both of which are routinely underweighted during contract review:

- Independent Contractual Status: An indemnity provision is treated as a separate, severable contract from the underlying agreement in which it is embedded. This principle was affirmed by the Himachal Pradesh High Court in H.P. Financial Corporation v. Pawana and subsequently reiterated by the Supreme Court of India in Deepak Bhandari v. HPSIDC. The clause operates under its own enforcement logic rather than as a mere remedy for a breach of contract.

- Anticipatory Crystallization of Liability: An indemnity holder’s right to relief can be triggered before they have sustained an actual out-of-pocket expenditure. Since the landmark ruling in Gajanan Moreshwar Parelkar v. Moreshwar Madan Mantri, Indian courts have established that where an indemnity holder has incurred an absolute liability, they may compel the indemnifier to discharge that liability directly. This anticipatory character means a mutual indemnity is a live asset protection threat that can be leveraged the moment a third-party liability becomes fixed, rather than a distant, contingent concern.

Mutuality guarantees nothing more than the existence of reciprocal promises. It does not ensure equity across the three critical operational variables like scope of triggers, liability caps, and procedural defense mechanics.

The Three Hidden Asymmetries of Mutuality

Asymmetry I: Symmetrical Language, Asymmetrical Triggers

While the grammar of a mutual clause may mirror perfectly across both parties, the operational realities of their businesses often collapse this symmetry.

Consider a SaaS provider licensing software to an enterprise customer under a mutual framework:

| Contractual Party | Reciprocal Indemnity Trigger | Actual Operational Risk Surface |

|---|---|---|

| SaaS Provider (Vendor) | Breach of contract, negligence, or IP infringement. | Intellectual property infringement in the codebase, systemic data-security failures, regulatory non-compliance, and cross-border confidentiality breaches. (High-frequency, catastrophic risk) |

| Enterprise Customer | Breach of contract, negligence, or IP infringement. | Failure to remit service fees or unauthorized deployment of the software beyond licensed seats. (Low-frequency, predictable credit risk) |

The vendor underwrites a systemic, uncapped portfolio of third-party operational risks, while the customer underwrites a basic billing invoice. The label “mutual” frequently misleads the party bearing the disproportionate operational load into abandoning negotiations on protective carve-outs, caps, and defense control under the mistaken impression that parity has been achieved.

Asymmetry II: The Unpriced Defense Obligation

Most commercial agreements conflate two distinct legal obligations into a single phrase: the obligation to indemnify and the obligation to defend.

- The Duty to Indemnify: A retrospective, back-end reckoning. It requires reimbursement only after a loss is legally established or an absolute liability crystallizes.

- The Duty to Defend: A prospective, front-end obligation. It requires the indemnifier to fund and conduct the legal defense from the moment a claim is merely alleged, long before any finding of liability is determined.

In an asymmetric risk relationship, a “mutual defense obligation” compels the party with the larger operational risk surface (typically the vendor) to finance extensive legal defense maneuvers based on mere third-party demand letters, even if the underlying claims ultimately prove meritless.

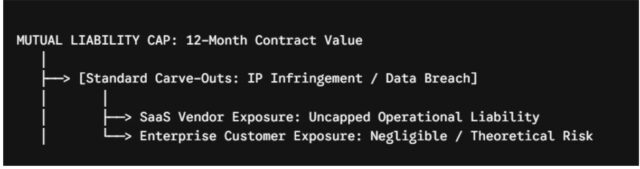

Asymmetry III: Caps and Carve-Outs

The interaction between liability caps and indemnity carve-outs is where risk asymmetry is permanently structured into an agreement.

Parties regularly agree to a mutual liability cap such as the total fees paid over the preceding twelve-month period and concurrently negotiate standard reciprocal carve-outs from that cap, such as intellectual property infringement, data privacy breaches, and confidentiality violations.

Because these carved-out categories map exclusively to the operational risks of the vendor, the clause becomes effectively uncapped for one side while remaining strictly capped for the other.

Furthermore, the relationship between the indemnity provision and the general limitation-of-liability clause must be structured to ensure the indemnity does not completely override the general cap. Indian courts enforce contractual caps strictly; in Bharati Knitting Co. v. DHL Worldwide Express, the Supreme Court held that parties are bound by the clear terms of a limitation clause even if the actual loss sustained far exceeds the contractual ceiling. Consequently, what a cap excludes via carve-outs is legally more consequential than the numerical limit itself.

Enterprise Maturity and Escalated Risk Profile

The risk associated with cosmetic mutual indemnification increases as an enterprise matures. This escalation is driven by three distinct factors:

- Asset Exposure: Early-stage, pre-revenue startups often present an uncollectible target for litigating third parties. Conversely, an established company with recurring revenue, an institutional cap table, and a funded balance sheet possesses valuable assets. Uncapped indemnity obligations represent material contingent liabilities that must be disclosed during financing rounds or M&A due diligence.

- Counterparty Scale: As an enterprise scales, its counterparties transition from fellow startups to enterprise-level corporations backed by specialized procurement teams. These sophisticated actors deliberately utilize cosmetic mutuality to secure lopsided risk allocations, knowing their internal legal departments can out-litigate smaller vendors.

- Boilerplate Complacency: Increased transaction volume frequently breeds executive complacency. Experienced operators who routinely encounter the phrase “mutual indemnification subject to a mutual cap” are more likely to skim past these provisions, inadvertently executing a high-risk liability structure.

Conclusion

Mutuality is a structural characteristic of drafting, not an equitable distribution of operational risk. An indemnification clause can be flawlessly reciprocal in its grammar and deeply unequal in its economic consequences. To protect corporate enterprise value, founders and operators must look past the word “mutual” and explicitly evaluate the scope, caps, and procedural mechanics of the clause.

Frequently Asked Questions

No. Mutuality only dictates the structural direction of the promises—meaning both sides have agreed to indemnify each other under the same linguistic framework. It says nothing about the actual commercial risk surface of each business. For example, in a SaaS contract, a vendor’s mutual indemnity covers systemic risks like IP infringement and data breaches (potentially catastrophic, high-value claims), while the customer’s reciprocal indemnity effectively only covers non-payment of invoices. The grammar is identical; the financial exposure is completely lopsided.

Section 73 limits recovery to direct losses that naturally arose from the breach or were reasonably foreseeable by the parties at the time of contracting, strictly excluding indirect, remote, or consequential losses. A bespoke indemnification clause operates outside these default statutory restrictions. If properly drafted, an indemnity can be engineered to capture consequential damages, indirect economic losses, legal defense fees, and regulatory penalties from day one, offering a far broader mechanism for recovery.

Under settled Indian jurisprudence (originating from Gajanan Moreshwar Parelkar v. Moreshwar Madan Mantri), an indemnity holder does not need to suffer an actual out-of-pocket financial loss before seeking relief. If the liability has become absolute and fixed (such as a clear third-party demand letter or an institutional assessment), the indemnity holder can legally compel the indemnifier to step in and discharge the liability directly to the third party or fund the defense immediately.

During negotiations, parties often agree to a comforting mutual liability cap (e.g., 100% of fees paid over the previous 12 months). However, standard boilerplate exceptions often carve out "IP infringement, data privacy breaches, and confidentiality violations" from this cap. Because these carved-out risks live almost entirely within the vendor’s operations and codebase, the vendor’s liability becomes effectively unlimited, while the customer remains completely protected by the original cap. The system looks symmetrical on paper but functions as an absolute liability trap in practice.

They are completely separate legal covenants wrapped into the same paragraph. The duty to indemnify is a back-end reckoning—it triggers only after liability is legally established or a loss is finalized. The duty to defend is an aggressive, front-end obligation that requires you to open your checkbook, hire lawyers, and fund a legal defense the moment a third-party allegation is served, regardless of whether the claim has any actual legal merit. If your business has a broad risk surface, a mutual defense obligation effectively forces you to underwrite your counterparty’s early-stage litigation costs.